Why Gold Lost Its Luster As Money

Story of the Gold Standard, why it collapsed, and could it have saved us from the COVID-19 pandemic.

Picture: Dan Dennis on Unsplash

It was a warm Sunday evening in Washington on the 15th of August 1971, when American President Richard Nixon announced that the US Dollar would no longer be redeemable to gold. This move effectively severed the last thread that connected money to gold.

For thousands of years, gold was used as the preferred form of money by many civilizations. The world went from literally using Gold coins as money to a Gold Standard or issuing paper currency notes redeemable in gold and then finally to the Bretton Woods system which eventually crumbled as a result of Nixon’s decision announced that August Sunday evening.

This is the story of how the yellow metal lost its luster in the monetary world.

Use of Gold coins in antiquity

Civilizations around the world have been intoxicated, obsessed, haunted, humbled, and exalted over Gold for many millennia¹. This readily malleable, highly dense yellow metal that is so incredibly inert that unlike other metals which lose their sheen to oxidation, a Gold ornament buried under the ground of a five-thousand-year-old archaeological site would shine just as bright as it did when it was adorned by an Egyptian royal.

Gold has been used in many civilizations across China, India, Turkey amongst other places for thousands of years. Coins were minted out of gold manually and under a monarch’s authority and seal. The Gold Standard was a commitment by the country’s government to fix the prices of their currency in terms of a specified amount of gold².

Countries like India where Silver was scarce than Gold, followed the Silver Standard for a long time. But in most economies, Silver often played Gold’s trusted sidekick in what is known as a Bi-metallic standard where high-value coins were made of gold and low-value coins were silver. The value of each coin against Gold or Silver was fixed and was known as the Mint value. For example, the government may fix the Mint value of 1 gram of gold to be $1 and 1 gram of silver to be 1 cent. This would imply that the exchange value of silver to gold at the mint is 100:1. Now since Gold and Silver also had a commodity market, their market rates often swayed and that is when the government had to intervene and buy either metal at a price much higher than the mint price or adjust the mint price to reflect the market price in order to restore parity.

England followed the bimetallic standard but switched to a de facto gold standard in 1717. The United States switched from a bimetallic standard to a de facto gold standard in 1834 and officially switched in 1900.

Advantages of the Gold Standard

For any economy using the Gold Standard, the money supply is restricted by the amount of gold that the central bank or the government treasuries have in their reserve. This is because paper notes and other government securities are fully and freely convertible to those reserves. Bearers of these notes or securities can redeem them with the government for an equivalent amount of gold.

So whenever a huge amount of gold was discovered in the eighteenth and nineteenth-century leading to a Gold rush in California, Australia, or South Africa, the monetary system would receive a shock. Although the amount of gold in the system spiked in the short term, productivity i.e the number of goods and services produced remained the same. This would act as a natural monetary easing which would lead to increased spending which in turn caused a rise in prices as the output of real goods had not changed. Thus even though the gold rushes upset the system from time to time, it never caused long-term inflation.

Because the government was not allowed to pump an excessive amount of currency into circulation for any reason(as long as the gold to currency exchange ratio remained constant), the era of the Gold Standard witnessed relatively stable and close to zero or negative inflation rates.

Picture: US Annual Consumer Price Inflation, 1880 to 2016 (Source: Federal Reserve Bank of Minneapolis)

When two countries followed the Gold Standard, because their currencies were pegged to the same commodity, their currency exchange rates were more or less fixed which reduced foreign exchange risk and reduced the cost of doing cross-border trade.

With inflation in control and a stable currency exchange environment coupled with increased output and foreign trade due to industrialization and new sources of raw material from the new world and Africa, we observe an unprecedented increase in output and prosperity in the independent industrialized countries like the United States and the European Imperial powers between the 1870s until the World War I. Countries occupied by the British, French, and Dutch as colonies of course did not benefit from this and in fact, became poorer as Europe grew richer.

World War I and the breakdown of Gold Standard

As the Great War broke out in Europe, many countries faced mounting war bills and desperately needed liquidity which the Gold Standard did not allow for. So many countries engaged in the war took their currencies off the gold standard and started freely printing money. This resulted in high and in some cases hyperinflation, which lingered around and in fact exacerbated after the war.

The United States had loaned money to the Allied powers during the war and demanded payback. The Allied powers were broke themselves and relied on the huge reparation payments that were forced upon Germany and its allies in the Treaty of Versailles after the war. The vanquished nations had no gold left in their coffers and their economies were exhausted. The US finally lent money to them so that they could pay reparations to the Allied powers which in turn owed money to the US. To break this vicious cycle the US had to eventually cancel its remaining debt to its Allies.

The Interwar period

After the war ended, the Gold Standard was reinstated at the pre-war exchange rates but the reality was now very different. Britain’s economy was not what it used to be and so naturally the Pound Sterling was nowhere close to its pre-war exchange rate against the US Dollar. Due to its inflexible approach towards money supply, the Gold Standard had failed to withstand the pressures of a crisis.

Toward the end of the 1920s, the Great Depression hit due to a combination of economic and monetary factors. Unemployment, hyperinflation, and a drop in productivity reached record levels and prevailed for many years. Global cooperation and free trade that had helped countries only a decade ago to prosper were forgotten and closed trading blocs emerged. Distrust, protectionist strategies, and beggar thy neighbor policies soon set the stage for the second World War.

Bretton Woods

After D-day marked the beginning of the end of World War II, delegates from forty-four countries convened in July 1944 at Bretton Woods, New Hampshire in the US to discuss the road to global economic recovery. With barely a scratch from the war on its soil, the US was the only major economy left standing and had once again emerged as the biggest lender to the world. All other countries were both out of Gold and US Dollars to repay their debts. So a modified form of the Gold Standard was created. Since the US already held a disproportionate amount of Gold in its coffers, it was proposed that the US Dollar would be pegged to Gold while all other countries would peg their currencies to the US Dollar.

Picture: John Maynard Keynes at the Bretton Woods conference with other delegates(Source: The Economist)

Other than the new monetary system, the Bretton Woods system designed primarily by British economist John Maynard Keynes also proposed the creation of two new organizations — The International Monetary Fund (IMF) and the World Bank. The IMF was formed to monitor exchange rates and help nations that needed global monetary support. The World Bank was created to provide loans to countries that had suffered from the war.

For Europe, Japan, and many other countries around the world reeling from the aftermath of the war, this new system meant that to grow their economies, they needed more and more US dollars. This was possible by running a trade surplus which would mean producing more and more which in turn needed capital. If a country did not have enough capital, the only source was foreign, more specifically US aid.

Marshall Plan

In June 1947, George Marshall presented America’s plan to give additional economic aid to Europe. The offer was open to all of Europe, including wartime enemies and the Communist countries of Eastern Europe. Almost $13.6 billion dollars were handed out as part of this plan. But the help came with strings attached. Countries who wished to receive aid under the Marshall Plan had to ensure that they increase their exports to the US, amongst other conditions.

Europe and Japan made a miraculous economic recovery in the early 1950s and the Bretton Woods system with help from the Marshall Plan and increasing military spending abroad by the US seemed to be working.

Booming global productivity meant that the monetary reserve of countries had to expand to ensure sufficient liquidity. Other countries started stockpiling the US dollar and the US needed more and more Gold to satisfy this need. Gold mining alone could not have satiated this hunger for gold.

In order to maintain global liquidity and remain the world’s reserve currency issuer, the US needed to run a balance of payment deficit by printing dollars beyond what its gold reserves permitted and spending them more abroad than at home in the hope that those countries wouldn't redeem their dollars for gold. This lead to rising inflation in the US.

Bank Run on the Great American Gold Reserve

In 1966, foreign central banks and governments held over 14 billion U.S. dollars. The United States had $13.2 billion in gold reserves, but only $3.2 billion of that was available to cover foreign dollar holdings. The rest was needed to cover domestic holdings. If governments and foreign central banks tried to convert even a quarter of their holdings at one time, the United States would not be able to honor its obligations³.

Since the Pound Sterling was also used in small measures by some countries as the reserve currency when the US dollar was in short supply, Britain was also in a similar position as the US. A persistent balance of payments deficit finally forced Britain to devalue the pound in 1967. Speculation ran amok that the dollar might soon follow suit. Private holders of the US dollar flocked to exchange their dollars for gold. To stop this uncontrolled outflow, the US suspended redemption of dollars for gold in 1968 for private parties. Only central banks were allowed to redeem their dollars at a fixed rate of $35 per ounce. In May 1971 however, even the central banks began to redeem their dollar reserves. America's gold reserves were fast dwindling. If this ‘run on the bank’ redemption continued, not a single bullion would be left in America’s vault!

No more pegged to Gold

As a response to the decade-long domestic inflation and the gold drain and to maintain the US dollar’s position as the world’s reserve currency, President Nixon announced on 15th August 1971 that the US dollar would no longer be redeemable for Gold by private parties or foreign Central Banks⁴. The dollar had now become a Fiat currency- inconvertible paper money made legal tender because the government says so.

For thousands of years, the idea of money was that it is something tangible, its value derived from something physical and valuable, and hence its availability limited by what the earth can provide. With the world moving to Fiat money standard, there is now no limit to how much money can be created when required(and sometimes even when not required).

Following the US decision to abandon the Gold peg, the rest of the world abandoned the security and discipline of a fixed-rate metal standard and adopted a system of “floating” exchange rates where each currency’s value moved up or down depending on international demand and the amount of confidence in its country’s economy⁵.

Although this one pillar of the Bretton Woods system was taken away, the IMF and the World Bank are still very much operational, and in fact, the IMF plays an even more important role now that foreign exchange rates are floating. Even though the Gold Standard was abandoned, central banks around the world still hold Gold in their reserves and the yellow metal continues to remain valuable to people.

COVID-19 and Gold Standard

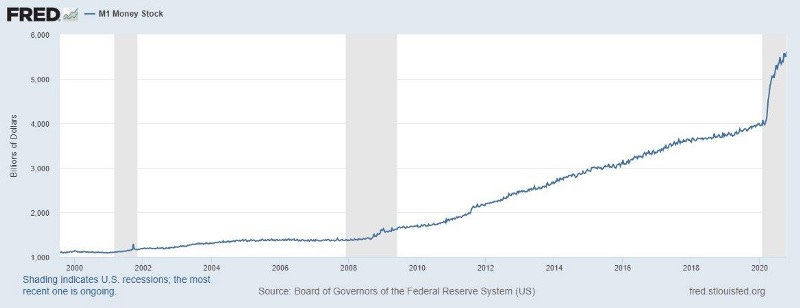

It may appear that if World War I not happened, the 40 year-long periods of prosperity fueled by the Gold standard would have continued and we may still have been using it. But I don't think that is true. All bull runs eventually end and all economies eventually take a cyclical downturn. Even if there was no World War, there still would have been natural calamities, pandemics, banking system collapse, or many other reasons for which there would have been a need for additional liquidity which the Gold Standard just cannot provide. Imagine if we were on the Gold Standard at the beginning of 2020. When the COVID-19 pandemic hit and the world had to shut down, most central banks injected liquidity to save the economy by using a method called Quantitative easing or as the media likes to call it- ‘Creating Money out of thin air’, which is not possible when the currency is pegged to a commodity. Since the pandemic started in March this year, the M1 Money stock in the US has increased by roughly 2 trillion dollars in six months even though productivity came to a virtual standstill.

Money Stock [M1] (Source: FRED, Federal Reserve Bank of St. Louis)

This liquidity injection helped the economy tide over the slump which wouldn’t have been possible in the Gold Standard. But if the Central bankers miscalculate, this kind of pump and dump can very easily trigger inflation which may be difficult to climb out of. The world can only hope the bankers don't get it wrong. The price of Gold in the commodity market saw a jump this summer as a lot of people wanted to hedge against this tsunami of liquidity by running to the safety of gold.

“We have gold because we cannot trust governments.”

- US President Herbert Hoover, 1933

References

[1] Peter L. Bernstein- The Power of Gold, The History of an Obsession

[2] Michael D. Bordo- Gold Standard, The Library of Economics and Liberty

[3] Money Matters: An IMF Exhibit — System in Crisis (1959–1971)

[4]Michael D. Bordo-The Imbalances of the Bretton Woods System 1965 to 1973: U.S. Inflation, The Elephant in the Room

[5]Money Matters: An IMF Exhibit — Reinventing the System (1972–1981)

You just read the sixth essay in the series ‘An Inquiry into Money’.

If you enjoyed reading this post, do come back next weekend.

If you haven’t yet, subscribe now to have these essays delivered to your inbox and tell your friends about it.

I also publish this series on Medium.